Fenix Resources (FEX): 900%+ Upside Potential in Iron Ore

At first glance, Fenix Resources (FEX) is a high-cost, single-asset Australian iron ore producer with a low remaining mine life (<4 years). And with a $150M market cap, most investors stop there and move on to the next idea.

The good news is that they’re wrong.

FEX is not just a single-asset producer of ~1.3Mt/year. It's a company in rapid transformation, expanding into a four-mine operation that will generate 4Mt+/year of iron ore at $50/t+ margins. And that’s not all.

The company also owns a mining logistics business and was recently awarded a $70M contract from just one customer (not to mention its ~ $50M replacement cost value).

Additionally, FEX owns irreplaceable port infrastructure assets in Geraldton, which help deliver bulk commodities globally from Mid-West Australia. The port assets have between $80 and $150M in insurance-backed replacement value.

Finally, the company has ~$25M in net cash on the balance sheet and has paid $45M in cumulative dividends since 2022. Company insiders also own 13% of the business.

FEX has over 900% upside from the current stock price. But before we dive in …

Quick housekeeping note: Enrollment into our Collective is open until the end of this week.

The Collective includes all of our research, a full library of reports and videos on theory and strategy, our proprietary market dashboard, plus our internal slack where the team and I, plus fund managers and die-hards from around the world talk shop, exchange ideas, and shoot the shit.

We’re having a decent start to the year with our book up +38% YTD.

If you’re interested in joining our crew, just click the link below. I'm looking forward to seeing you in the group.

Alright … back to the stock.

The mining business will generate ~$180M+ in pre-tax profits at scale. At a 5x multiple, it’s worth $940M ($1.36/share).

If FEX captures 7% of its local market, its logistics business can generate $160M in annual revenue. Assuming 12% margins and an 8x multiple, logistics is worth $157M ($0.23/share).

The tangible port and logistics assets are worth ~$133M or $0.19/share.

And finally, the $25M net cash is worth another $0.04/share.

Total potential upside: $1.84/share

Current share price: $0.21/share

FEX’s Mining Business: From 1 → 4 Producing Assets

FEX currently has one producing asset called Iron Ridge. It’s a world-class iron ore mine with 65% Fe grade in a Tier-1 jurisdiction (Mid-West Australia).

The mine produces ~1.3Mt/year and has ~3-4 years of mine life left.

Iron Ridge is a high-cost mine at ~$54/t compared to Vale’s (VALE) $30/t or Rio Tinto’s (RIO) $24.5/t. However, the company generates $50/t+ in profit at historical average iron ore prices through a) controlling costs (see below) and b) selling their ore at a premium to market (given the higher grades).

The company says it will explore Iron Ridge further, but I’m assuming $0 for that exploration and that the mine will run out after its remaining mine life.

At 20YR historical iron ore prices, Iron Ridge generates ~$60M in pre-tax profits (or 49% of the current EV).

But the market already knows about Iron Ridge. What it is not valuing are the company’s other expansion assets.

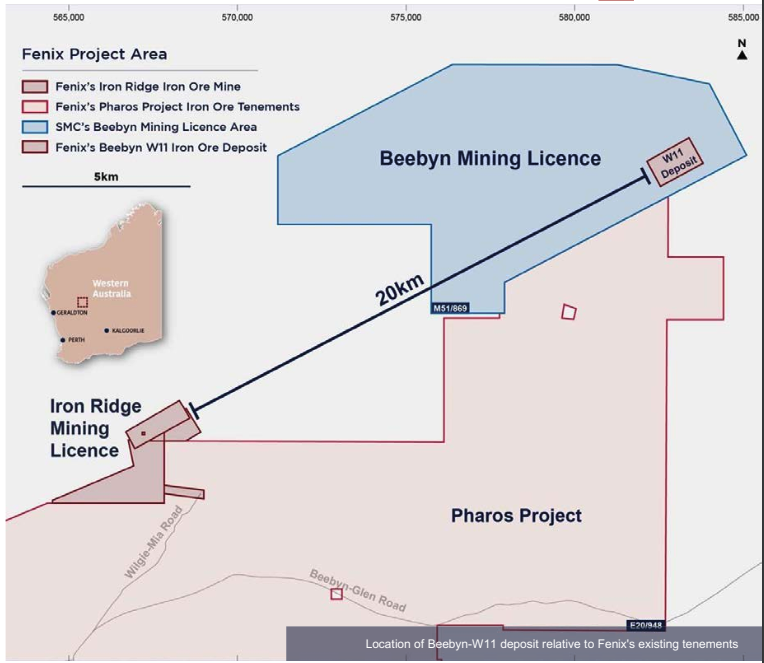

Beebyn-W11 Iron Ore Deposit

In October 2023, FEX acquired the “right to mine” 10Mt of 61.3% Fe iron ore from Sinosteel.

There’s a lot to like about this deposit.

First, it’s high-grade at 61.3% Fe and could command a market premium (like Iron Ridge).

Second, it’s only 20km from Iron Ridge, so FEX can share existing infrastructure/leverage its logistics business to reduce cash costs.

Finally, Sinosteel has an additional 10.4 Mt of 61.3% iron ore for mining. If things go well on the first 10.1 Mt, Sinosteel would agree to give FEX the remaining 10.4 Mt. However, I only use the initial 10.1 Mt in my valuation and life estimates.

Let’s do some basic math on the W11 deposit earnings potential. I assume production will look like Iron Ridge, so 1.3Mt/year with slightly higher cost structures ($60/t).

At $100/t iron ore prices, the W11 deposit generates $130M in annual revenue and $52M in pre-tax profits (or 42% of current EV) with an initial mine life of 4.7 years.

Shine Iron Ore Project (Acquired from Mt. Gibson at Distressed Prices)

In July 2023, FEX took advantage of the 2021 decline in iron ore prices and rising shipping rates by purchasing the Shine Iron Ore project from Mt. Gibson.

The company paid $6.72M in cash plus 60M fully paid FEX shares for a (true!) shovel-ready project with $40M+ in sunk costs 230km east of Geraldton port.

Here’s what FEX got for its ~$34M investment:

15.1Mt of 58% Fe

Open pit, shovel-ready project with similar cash costs to Iron Ridge

Estimated ~$200M NPV at $87/dmt iron ore prices

According to recent investor presentations, the Shine Iron Ore project’s cash costs and annual production should look like FEX’s Iron Ridge asset. Here’s what the economics look like under those assumptions:

Average annual revenue: $130M

Average annual pre-tax profits: $59M

Mine life: 6.7 years

Estimated EV Yield: 48%

Third-Party Artisanal Production: Twin Peaks

The final part of FEX’s production growth strategy is its third-party purchasing business (i.e., artisanal mining). We’ve covered third-party production via Andean Precious Metals (APM.V).

FEX bought 500Kt of 60%+ iron ore from 10M Pty Ltd’s Twin Peaks deposit. According to a recent CEO interview, the company paid ~$40/t for the ore, which it will sell under its Fenix brand.

This is the power of owning your logistics and infrastructure operations. FEX can go to smaller, sub-scale mines and say, “We’ll pay you $X for your iron ore, in exchange, we’ll provide discounts on logistics and shipping.”

It’s a win-win. FEX gains access to more iron ore, and sub-scale operators gain access to a reliable buyer … the small miner makes money, and FEX makes money.

I couldn’t find any data on the Twin Peaks mine, so my valuation includes the 300Kt generated by $30M in revenue and $18M in profits.

To understand the market opportunity for third-party production … FEX estimates that there are 100+ multi-commodity stranded projects in Mid-West Australia. FEX’s logistics and port assets unlock these projects with millions of ounces of profitable ore.

Again, my valuation assumes that FEX captures 0% of the 100+ available potential project ounces.

FEX’s Logistics Business: $70M Is Just The Beginning

FEX wholly owns its NewHaul logistics business after buying the remaining 50% ownership from NewHaul founder Craig Mitchell. Mitchell now runs FEX’s logistics business. Before the sale, Mitchell founded the Mitchell Group and grew it into Australia’s largest bulk haulage company.

The company provides logistics services through its various assets:

200-ton haulage vehicle fleet

Rail sidings/haulage for product storage

Inland port

Logistics depot

In March 2024, NewHaul won a three-year, $70M logistics services contract with Gold Valley’s Mid-West iron ore mine. The agreement covers 3Mt of annual iron ore haulage (or $7.78/t).

Investors prefer logistics businesses to mine production. The average logistics company generates ~12% EBITDA margins and can command an 8-12x multiple.

With this contract, FEX will generate $23M in annual revenue and $2.8M in EBITDA (assuming 12% margins). At an 8x multiple, the logistics business is worth ~$22M.

But that’s one contract. And we know that there are 100+ multi-commodity projects within Mid-West Australia.

Let’s assume FEX’s logistics business wins 7% of those projects at an average annual tonnage rate of 3Mt (or 21Mt).

Here’s what the logistics business could look like (see below).

At 21Mt/year, FEX’s logistics business would be worth $157M or $0.23/share. That’s $0.02/share more than the company’s current share price ($0.21/share).

Which you’re getting for <$0, thanks to FEX’s iron ore cash flow!

Downside Protection: Replacement Cost of Hard Assets

Downside protection starts with the replacement value of the company’s hard assets, namely its port infrastructure, logistics assets, and net cash.

Let’s start with the hard assets (see below).

Replacement costs for FEX’s rail sidings and port assets vary between $80M and $150M. For reference, CEO John Welborn recently ascribed ~$150M in replacement cost for the port assets and $50M for the rail sidings.

At $133M, FEX’s hard assets are worth ~$0.19/share or 89% of the current market cap. Add another $25M in net cash for $0.04/share, and you have ~108% of the current market cap in replacement value and liquid cash.

It’s also worth noting that the cash has value … John Welborn has said, “in a bad month the company generates ~$5M/month in free cash flow.”

FEX consistently adds net cash to its balance sheet, barring any investment capex or dividends/buybacks.

Putting It Together: 900%+ Upside

It sounds ridiculous… but the math is the math (see below).

Yes, I’m making many assumptions that will probably be wrong by some margin. But still, you have hard asset replacement values worth 90% of the current market cap and a net cash balance worth another 19% of the market cap.

In other words, you’re paying $0 for the following …

FEX’s mining business will expand from 1.3Mt/year to 4Mt/year, generating $50/t in pre-tax profits.

FEX’s logistics business will generate $23M/year in revenue at 10-12% margins from only one customer contract with 100+ potential projects within its direct vicinity.

There are a few things that kill this thesis.

The first and most apparent is iron ore prices. Lower iron ore prices mean lower profits and multiples. Iron ore prices have averaged ~$100/t over the past 15YR (see below).

FEX even makes money at a -1 Std Deviation price of $68/t.

The other thesis killer is share dilution. FEX has increased its share count from 109M in 2019 to 685M today. There are legitimate reasons for the share issuance … the company needed money to build Iron Ridge, bought Shine Iron Ore and the Mt. Gibson port assets, etc.

But at this point, we shouldn’t see dilution as a) the asset value is there and b) cash flow should increase substantially as the new mine production comes online.

Remember, management owns 13% of the company and is proud of the dividend payment. I don’t see management willingly diluting themselves and reducing dividends-per-share unless they see an investment greater than buybacks or increased dividends.

Conclusion: FEX Is An Incredibly Asymmetric Setup

I love asymmetric setups like FEX, especially when you have >100% of the current market cap backed by hard asset replacement costs and net cash on the balance sheet.

FEX is unique in that it offers massive downside protection and a transformational upside that the market has yet to recognize.

Over the past three years, the company went from a single-asset, high-cost iron ore miner to a multi-asset, 4Mt producer with port infrastructure and a wholly-owned logistics business.

We get this entire transformation for <$0. We currently have a starter position for 5% notional and will add on pullbacks.

I’d love feedback on this idea … tell me where I’m wrong and what I’m missing.

And before you go … remember to join us in the Macro Ops Collective!

The Collective includes all of our research, a full library of reports and videos on theory and strategy, our proprietary market dashboard, plus our internal slack where the team and I, plus fund managers and die-hards from around the world talk shop, exchange ideas, and shoot the shit.

We’re having a decent start to the year with our book up +38% YTD.

If you’re interested in joining our crew, just click the link below. I'm looking forward to seeing you in the group.