Andean Precious Metals (APM.V): Hunting For Value in Bolivia

Junior mining stocks are starting to break out. It’s about time for silver and gold prices to hit new relative and all-time highs, respectively.

Soon, you’ll hear mining stocks pitched on CNCB. Of course, that’s when the trade will have run its course, the easy money already made, and the “smart” investors out with their profits, searching for the next big trade.

At the end of 2023, we (the MO team) started becoming bullish on precious metals and precious metals mining stocks.

But nobody wanted to hear our gold and silver pitch. Nobody cared.

Yet we couldn’t ignore the value, cash flows, and shareholder returns we saw in some of these precious metals junior miners.

So, we wrote our ideas for our Macro Ops Collective members before anyone cared to listen. By year-end 2023, we bought a handful of junior precious metals miners.

And we’ve made a lot of money.

Those stocks have dramatically outperformed their respective benchmarks … the S&P 500 and NASDAQ 100. One has already returned over 100% YTD.

Over the next few days, we’ll share our initial write-ups on these companies.

You’ll see what we saw, read how we thought about the valuation, and learn how we pounced on what we thought was an obvious opportunity … Jim Rogers’s money lying in a corner.

If ideas like these get you excited, you should consider joining our Macro Ops Collective.

It’s a private investment community with former hedge fund managers, Market Wizards, and full-time traders. All trying to become consistently profitable while having a hell of a good time in the process.

If this sounds like your type of place, join us using the link below. We can’t wait to see you.

The first idea was on January 31, 2024.

—————————————————————————————————————————————-

Markets are mostly efficient at valuing securities. However, there are some corners of the market where no one is watching, and you can find a complete steal. Small-cap Canadian precious metals miners are one such hunting ground.

Enter Andean Precious Metals (APM.V).

APM is a Canadian mid-tier gold/silver producer. The company has two main assets: a silver mine/oxide processing plant in Bolivia and a gold mine in California.

Here’s why we bought the stock. APM trades at a $119M market cap with a Net Current Asset Value (or NCAV) of $107M. The company has $161M in net cash and equivalents for an Enterprise Value of -$42M.

In other words, the market values APM’s two producing mines and its silver mill at -$42M.

Combined, we think those two mines can generate over $30M in annual free cash flow by 2025 using realistic gold/silver price assumptions.

Finally, management owns over 50% of the business and has repurchased stock over the past year ($0.02 above our cost basis).

Got your attention? Let’s dive into the business.

APM has a simple business model. The company buys nearly depleted – but still producing – mines from larger operators for cheap. They then throw some money behind mine life expansion, add a few more years to production, and generate incremental cash flows at high rates on invested capital.

If that sounds familiar, it's because it’s nearly identical to Valeura’s (VLE) strategy. You can watch our webinar on VLE here.

Let’s start with the silver mine.

San Bartolome: A Strategic Asset For Cheap

APM bought the San Bartolomé silver mine from Coeur Mining in 2018. Coeur spent $190M building the mine and mill. I couldn’t find how much APM paid for the mine, but the company reported Gross Property, Plant, and Equipment of $84M in 2019 (farthest back for financials).

San Bartolome had ~8 months of production left when APM bought it in 2018. The company invested in exploration and added another 4-5 years of life to the mine. The result? From 2020 to 2021, the mine produced 5.9Moz of silver and generated $30M+ in annual free cash flow.

It’s important to note that the San Bartolome is home to the country’s only silver oxide processing plant. Which the market values at -$42M.

This processing monopoly allows APM to produce more ore from third-party sources (like smaller / artisanal producers) via a “cost-plus” business model.

For instance, the company signed two purchasing agreements last year. One for five years and up to 800,000t in Paca, and another in Alta Vista for 170,000t over the next 24 months.

Smaller producers win because they generate revenue and don’t have to spend millions of dollars building their own processing plants. APM wins because they can increase production while extending the mine life at San Bartolome.

The other added benefit is that APM can flex production at San Bartolome to match silver prices. If silver prices are low, they buy more from third-party producers. If silver prices are high, they produce more of their ore.

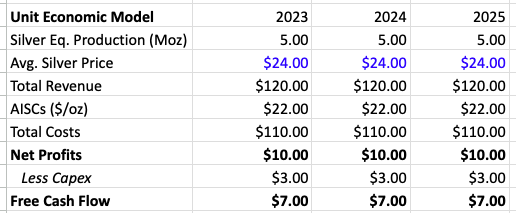

Modeling The Silver Mine

Here’s the back-of-the-napkin math on the San Bartolome mine over the next three years.

I assume the lower end of average silver prices and the higher end of AISCs. And I still get $10M in net profits and $7M in FCF per year. It’s mining, so everything could change. Higher silver prices should increase production, which helps leverage AISCs to generate more profits, etc.

If you assume we hit 2020 silver prices of $28/oz, San Bartolome would generate $27M in free cash flow per year.

Before exploring the gold mine asset, I want to emphasize one more thing about this silver mine/mill. San Bartolome is a critical asset for the country, specifically the mine’s home city. The mine accounts for 25% of the local GDP, and most townspeople work there.

And it’s the country’s only silver oxide processing plant.

Golden Queen: A Transformational Acquisition

Transformational acquisitions have become somewhat of an “Investment Theme” at Macro Ops.

Whether it’s Journey Energy’s (JOY) power plant acquisition or North American Construction (NOA) buying MacKeller Group. These purchases entirely change the company’s earnings power and, in turn, valuations.

APM completed a transformational acquisition in November by buying the Soledad gold mine from Golden Queen Mining LLC. Here’s how the company financed the deal:

$5M paid at closing

$7.5M loan payment paid at closing

$5M payable on 12-month anniversary

$5M payable on 22-month anniversary

$43.9M term loan due November 2025

An all-in cost of $66.4M.

Since its launch in 2016, the mine has produced 340,000oz of gold and 3.4Moz of silver.

The company estimates that the mine will produce ~50,000oz-55,000oz of gold per year with AISCs of $1,400-$1,600/oz. We’ll model the cash flow in a bit. But here’s what APM got for their $66M.

$2M in receivables

$79M in inventory (gold bullion)

$5M in supplies

$116M in equipment/infrastructure

$5M in restricted cash

Subtract total liabilities ($74M), and you have $133M in incremental NAV. APM came out of pocket for only $22.5M.

It’s a great deal on assets alone. But what about cash flow?

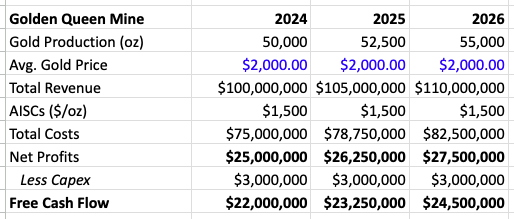

Modeling The Gold Mine

Here’s the back-of-the-napkin math on the gold mine over the next three years.

Capex for this mine should be low (probably below the assumed $3M/year) as Golden Queen spent $23M+ from 2021-2022 improving the mine and surrounding infrastructure.

At $2,000/oz gold, this mine should generate $22-$25M in annual free cash flow. Remember, APM purchased this mine with $22.5M cash down and $43.9M in debt.

In other words, if things go well, the mine pays for itself in two years, and APM has a debt-free gold mine generating $25M in annual free cash flow.

Bringing It Together: Combined Mine Cash Flows & NAV Valuation

APM’s mines can generate $30-$35M in annual free cash flow under reasonable precious metal price assumptions.

Moreover, the Golden Queen mine acquisition diversifies APM’s asset base and de-risks the “single mine” bear case. This should flip investor sentiment from valuing the company on a liquidation basis to a NAV basis.

Speaking of NAV, here is my reconfigured balance sheet post-Golden Queen acquisition (which should be reflected in the following quarterly earnings report).

The stock is a double at 0.50x NAV and nearly a four-bagger at 0.75x NAV.

In the meantime, APM will earn 25% of its market cap in free cash flow annually while we wait for market prices to catch up with asset values.

Stocks are usually cheap for a reason, so why are we so blessed to find APM?

First, it’s a small-to-micro-cap Canadian precious metals producer. That alone is reason enough. Second, it’s relatively illiquid. Third, nobody likes precious metals. They’re not as sexy as battery metals like lithium or industrial metals like copper.

APM provides serious torque to higher gold and silver prices. But it also offers tremendous downside protection in the form of fixed assets, high insider ownership, a buyback for 5% of the stock, and liquid assets (cash + gold/silver bullion) worth more than the entire market cap.

It’s like this. Suppose I had a box. Inside that box was a $30 gift card that automatically replenishes every year. If I said, “I’ll pay you $42 to take this box off my hands. Oh and by the way, the box is worth anywhere from $106 to $500.” Would you take the deal?

It’s ideas like these that get me excited to wake up every morning.