Macro Ops 2022 Performance Review (Part 1)

At the end of every year, we (the MO team) spend a couple weeks dissecting last year’s trading performance. We analyze what did/didn’t work, and hopefully come away with some valuable lessons to up our game in the new year.

This was a tough trading year, especially for our type of trading that seeks to capture significant market trends. Instead of trending markets, we got a whipsaw bear market. We made many mistakes and unforced errors.

Yet despite these blunders, we returned over 10% while the S&P 500 returned -18%. Since 2020, the Macro Ops portfolio has returned 83% (27% CAGR) compared to the S&P 500’s 18.50% total return.

So as frustrating as this year was, it could’ve been much worse.This is a two-part essay. In part one, I (Brandon) dive deeper into the quantitative performance metrics. We discuss things like:

Monthly and quarterly returns

Returns by asset class

Biggest individual winners/losers

I then unpack three critical lessons from our equity trading this year, including:

Matching trade management timeframes with our investment horizon

The perverse incentives between running a newsletter and running a portfolio

Changing my game when the rules change

In part two, Alex dissects the broad Macro Calls we made during the year. He breaks down why we made them, how we represented them in our portfolio, and what we could’ve done to improve our returns based on those convictions.

He then dives deeper into our futures, forex, and crypto trades – the stuff that made our year profitable – to see what went right and the lessons we can take from those successful trades.

As we mentioned above, this was a challenging trading year. At one point, we were up over 30%. We thought about selling everything, taking a beach vacation, and waiting for 2023. Maybe we should listen to that little voice in our heads next year.

We hope you enjoy this 2022 Macro Ops Performance Review.

Part 1: Quantitative Return Breakdown & Equity Trading Recap

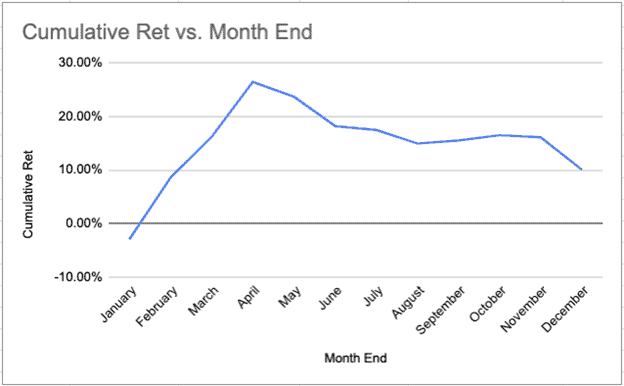

The MO Portfolio returned slightly over 10% in 2022. You can see the cumulative return chart below.

I’m not gonna lie; by the end of April, we thought a triple-digit year was ours to take. You know how the saying goes, “you plan, and the Market Gods laugh.”

April turned out to be the peak for returns. From there, we suffered an eight-month drawdown that expended more mental capital than physical.

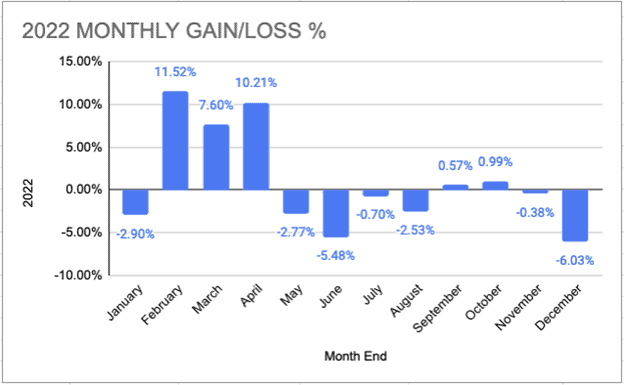

Here’s a monthly breakdown of our returns (see below).

We lost money in seven of the twelve months. Our average loss in losing months was -2.97%, and our average gain in positive months was 6.20%.

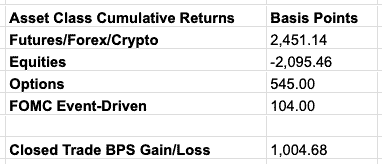

This year's most surprising data point was our asset class returns (see below).

We generated +24.51% from our futures, forex, and crypto trades. However, we lost 20.95% from our equity book.

Our biggest winners in the equity book were:

VIST: +293bps (four trades)

We first started buying VIST in the low $6s. We traded around our core position throughout the year and saw VIST rise over 100% from our initial cost base.

POWW: +269bps (two trades)

POWW was one of our biggest winners in 2021, and we squeezed the last few drops of profit in 2022. We exited the rest of our POWW position at around $5/share. Our average cost basis was $2.75/share (~100 % + gain from cost).However, more important than our gain was that we exited before the stock cratered below $2/share. You can read more about why I changed my mind about POWW here.Our biggest losers were:

MSOS: -209bps (two trades)

NWBO: -165bps

LDO: -130bps

We didn’t experience many significant losses in the equity book (i.e., anything over 200bps). Instead, we suffered many more minor 40-65 bps losses or the “Death by a thousand paper cuts.”

MSOS rug-pulled us twice this year on “buy the rumor, sell the news” events.

NWBO was a position sizing error that caused a 65 bps greater loss than expected. And LDO was from a daily close well below our initial risk point.

I made a ton of mistakes in our Equity Book this year. And after spending a couple of weeks thinking about them, I came up with three main lessons learned from my mistakes. There’s nothing wrong with making mistakes. So long as you correct them over time and stop repeating past ones.

Here are the three main lessons I learned from our Equity Book in 2022.

Lessons Learned Trading Equities in 2022

Lesson 1: Matching Time Frame w/ Investment Horizon

One of our biggest mistakes in our Equity Book was mismatching our trade management time frame and investment thesis horizons.

For example, we’ve had a long-term energy bull thesis since late 2020-early 2021 (coal, oil, etc.) and bought a lot of the names that killed it this year (BTU, TDW, VIST, etc.). However, we entered and managed those positions using the daily chart.

We got stopped out in a bunch of names that, by year-end, were substantially higher than when we first bought them. That’s because we managed the trade in a different time frame than our investment horizon. One idea we have this year to prevent that issue is using longer-term charts on longer-term theses. For example, if we have a long-term (2-4 years) theory on something, we’ll manage it using weekly and/or monthly charts.

We're doing some work and backtesting on this front to better align positioning with views and conviction while tightly managing risk first.

This alignment between trade management and investment horizons reduces noise when we’re long-term bullish on a specific corner of the market. While simultaneously allowing for tighter risk management on shorter-term trades.

Lesson 2: Align Portfolio & Newsletter Incentives

Managing an online newsletter and a portfolio are very different, with opposing incentives sometimes.

We spend all day researching and writing about markets and new ideas. With that comes a magnetic pull toward action. A desire to always be doing something in the markets. If you’re not doing something, you can quickly think, “why is the reader paying me for research and idea generation if I’m not trading on it?”

Then, when you can’t take the feeling of doing nothing anymore, you overtrade and lose more mental and physical capital.

Running a portfolio is different.

As a portfolio manager, you're incentivized to 1) not lose money and 2) find the highest asymmetric risk/reward opportunities to make money.

Sometimes that means sitting on your hands and doing nothing for weeks or months. Other times it means aggressively trading when the getting’s good and eating as much meat off the bone as possible.

The “Holy Grail” (if there is one) between running a newsletter and a portfolio is learning to do “something” that adds value without adding unnecessary transactional costs.

There are a few ways to accomplish this:

Focus most of my time on companies I’ve already researched to understand them more deeply.

Write Industry Deep Dives if there’s nothing to do in markets (like 2022).

Only write about individual companies that are either breaking out of Stage 2 bases or are already in an existing uptrend showing relative strength.

Spend more time reading books and writing in-depth book reviews.

If I want to do nothing, I focus on industry deep dives or book reviews. And if I find an interesting idea, it should at least be something actionable that’s breaking out or showing above-market relative strength.

These rules create a flywheel between the newsletter and portfolio management by better-aligning incentives towards one goal: provide the highest quality value on the things that matter most.

Lesson 3: Change My Game When The Rules Change

2022 was when the market stopped obsessing over “growth at all costs” and demanded positive earnings and free cash flow. High-growth names got slaughtered as revenue multiples plummeted from 20x+ to low single-digits.

In other words, the rules of the game changed.

Instead of changing my game with the market, I stubbornly plowed forward, researching one high-growth, loss-making company after another.

That time would’ve been better spent exploring the things working in markets, like oil, energy, commodities, or traditionally “cheap” businesses. These stocks had fantastic charts, excellent fundamentals, and strong industry tailwinds. Yet I ignored them because I couldn’t kill my sacred, high-growth cow.

The best way to remedy this issue in 2023 is to only focus on what’s working in markets. Focus on the stocks/industries showing the highest relative strength and spending all my time learning about those businesses and setups.

Finally, 2023 is the year of No Sacred Cows. Say it with me, “I will not find my identity in any one investment/trading style.”

Getting Personal: What Were The Sources of My Errors?

The three lessons above reflect my growth from my (many) mistakes throughout the year.

Writing about your failures is a vulnerable exercise. That said, a year without embarrassment is a year without growth. So let’s get personal.

My Biggest Analytical Error: Not Going Deep Enough on Industry Research

Initially, my most significant error was misjudging the width of my circle of competence. And that was partly true. But the issue was deeper than that. Misjudging the width of my circle of competence stemmed from my false assumption about the amount of information I needed to make an informed decision.

Instead of digging six feet deep, I dug two-foot trenches and pitched my investment. I didn’t develop the solid foundational understanding of a company’s industry that I needed to form a high-quality opinion on its stock.

Part of the reason for this error is the fast-moving nature of publishing ideas online. I constantly felt pressured to find new stocks in new countries operating in new industries. “That’s how I’ll differentiate from the rest,” I told myself.

So I’d dig two feet in one place and write a half-baked thesis. Only to move on to the next shiny object, dig another two-foot trench, and repeat the cycle.

I valued pitching a new ideaover deeply understanding an industry.

But why did I do that? If I pull the onion back further, I realize it's because I’m desperately trying to play “knowledge catch-up.” I’m trying to compress 20-30 years of investment experience into the shortest possible time. And I tell myself that the best way to do that is to study (and write about) as many new companies as possible. But what if my assumption was wrong?

What I should do instead, and what I plan on doing in 2023, is study the big things that matter. That means spending more time learning about industries, the history of the competitive landscape, unit economics, capital cycles, barriers to entry, etc.

I’m excited to share my new research process with you this year.

My Biggest Weakness: The Crutch of Technical Risk Management

We use technical stop losses in our trading at Macro Ops. It’s one of the ways we differentiate from the conventional “value investing” community.

However, I’ve noticed that I use our technical risk management as a crutch for deeply understanding (and articulating) an investment’s downside risk.I tell myself, “It’s fine if I don’t really know the downside here, because we’ve got a stop-loss anyways.”

And that’s partly true. Stop losses prevent us from blowing up our account in one position. But it also stunted my growth as a value investor. Think about actual crutches. If I hurt my ankle but never got rid of my crutches, all those muscles would atrophy. My ligaments would freeze, and I’d lose all mobility.

My ankle would be useless.

I can say the same for stop-losses. If I constantly underwrite my investments with stop-losses in mind, I’ll never use my downside protection muscles. And what does that look like?

I stop asking, “so what?”

I relax my valuation criteria because there’s no penalty for overpaying

I pay less attention to balance sheets or replacement values

In other words, I lose all the value-investing muscles I gain from doing the deep work. I forget how to ride the bike without training wheels.

I told you this would be embarrassing to write, and it is. But it’s an honest reflection of where I’ve messed up over the last year. And by sharing these painful lessons publicly, I gain a sense of accountability that you can’t get without sharing my mistakes.

Conclusion: Back To The Basics

I’m touting 2023 as the “Back To The Basics” year. The path toward generating alpha from our equity book is simple but challenging. However, the lessons I learned in 2022 and the rules I’ve implemented for the upcoming year will help us turn our Equity Book from a headwind to a tailwind.

To recap, we’re spending 2023 focusing on the following:

Matching our trade management time horizon with our investment thesis horizon.

Aligning the Newsletter and Portfolio Management incentive structures to produce the highest quality and most valuable work possible.

Changing my game when the rules change and killing all sacred cows.

Tomorrow we'll be sharing Alex’s Futures, Forex, Crypto, Options, and Macro recap. Keep an eye on your inbox!

As we mentioned in the beginning of this review, 2022 was a very tough year to trade. We had to deal with a whipsaw bear market and a lot of investors got their portfolios trampled. Strategies that used to work in the previous bull regime fell flat during this more hostile environment.

In comparison, 2023 is setting up to be very interesting with multiple new macro shifts. The key to survive (and thrive) is to have a deep understanding of these changing market dynamics along with a flexible and robust strategy that can profit from them. Investing in equities alone won’t work anymore.

The best way to outperform in 2023 is to trade multiple asset classes and find different mechanisms to get exposure to hard assets. We’re staying flexible and fine tuning our strategies to better fit with the current landscape. If you want to prepare with us and tackle the opportunities this new year has to offer, then make sure to join our Collective.

A Macro Ops Collective subscription will grant you access to all our models along with the step-by-step instructions you need to create a bulletproof process for analyzing and profiting from the market.

We founded Macro Ops to foster as many high-level traders and investors as possible. Our goal is to share everything we know with our community, so we can learn and grow together while making a ton of money and creating positive change in the world. And of course, we want to have a helluva good time doing it all.

We accomplish this through better research, better process, and better training. That’s how hundreds of investors have already been able to consistently beat the market by implementing our investment process. You need the strategies, tools, and community that will support you through one of the most dangerous market environments we’ve faced in decades.

Join our team today.

We work day and night to filter the key information for you… to give you signals for when to pare back risk and when to go for the jugular… to give you the tools and process to excel beyond your peers… no matter if you’re a 20-year veteran hedge fund manager or a maniacally devoted recent MBA grad.

We exist to support your trading and investing success.

Join our team now and let’s crush these dangerous markets together.

Enrollment to the Collective ends Sunday, January 8th at midnight. Make sure you sign up before our doors close.