Jamie Mai's Trading Strategy Explained

Jamie Mai is a hedge fund manager who has generated world-class returns for Cornwall Capital, a fund he founded after studying history in college. Mai returned 42% per year for investors (net of fees) during the fund’s first nine years. $100,000 initially invested in Mai’s fund would’ve been worth $2,347,000 by the end of year nine.

Jamie Mai used multiple trading strategies to generate the fund’s returns, but they all shared a common thread. Jack Schwager explains it in his book Market Wizards(emphasis mine):

“The one unifying characteristic virtually all of Cornwall’s strategies share is that they are structured and implemented as highly asymmetric, positive skew trades—that is, trades in which the upside potential far exceeds the downside risk.”

The goal was to risk $1 to make $10. Mai understood that most of his bets would lose, but over time, the size of his winners would more than make up for those small losses.

Mai’s favorite way of expressing this strategy was through long-term, deep out-of-the-money options or DOTMs. For example, if a stock trades at $10 in 2001, Mai would buy the $40 calls dated for 2005. (If you want to brush up on options and volatility, we have a detailed report you can read here.)

DOTMs allowed Mai to risk small amounts of money in highly asymmetric bets. Here’s how he explains it in the book (emphasis added):

“Options are priced lowest when recent volatility has been very low. In my experience, however, the single best predictor of future increases of volatility is low historical volatility. When volatility gets very low in a market, we consider that a very interesting time to start looking for ways to get long volatility, both because volatility is very cheap in an absolute sense and because the market certainty and complacency reflected by low volatility often implies an above-average probability of increased future volatility.”

In layman’s terms, Mai used DOTMs to bet that a stock would go from barely moving to moving wildly higher or lower. To explain Jamie Mai’s trading strategy, here is a breakdown of three specific trades he made to generate outsized profits:

Jamie Mai’s Trade Examples & Strategy Explained

Trade #1: Altria (MO) Calls

In 2003, Altria, a major tobacco company, faced a wall of rating agency downgrades. This was due to negative developments in the multiple class action litigations against it. These cases carried the potential for large settlements in the billions of dollars. There was also the risk of setting a favorable precedent for future plaintiffs. This created significant uncertainty for Altria — bankruptcy was on the table.

Despite this uncertainty, Mai saw an opportunity in the out-of-the-money call options for Altria. So he placed his bet:

“So the first thing we checked was whether the Altria options still assumed a normal probability distribution, despite the presence of a bimodal event. Sure enough, the Altria option prices still implied a normal distribution, which meant the out-of-the-money options were way too cheap.

Since our work suggested a greater likelihood for a bullish outcome, we bought the out-of-the-money calls. The calls appreciated sharply when one of the key cases supporting the rating downgrades was thrown out on appeal shortly after we initiated our investment.”

Jamie Mai and his team made about 2.5 times their money on the trade and could have made even more if they held on longer.

The most important lesson here is just how mispriced bimodal events are in options contracts.

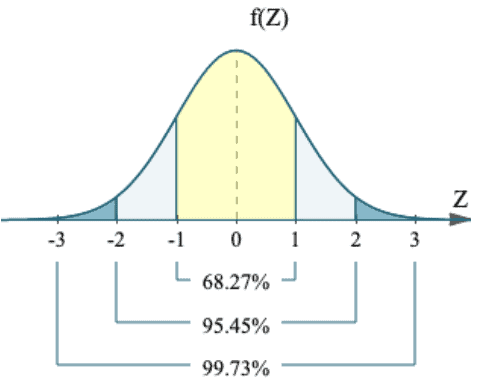

Most options assume a normal distribution of future price outcomes. This means they’re betting that the future price of a stock will most likely fall within one standard deviation of the current price. That’s why you get the normal bell curve distribution seen below:

Now this is true for most stocks. You’re not going to see wild swings in their price overnight. And the options market prices that efficiently with this normal distribution.

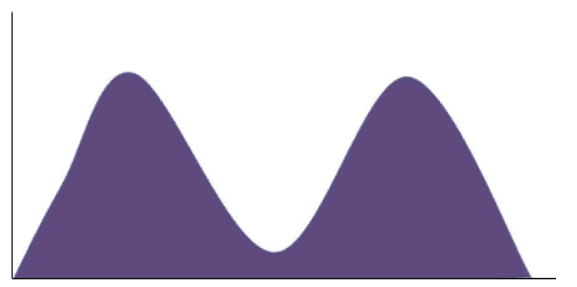

But this isn’t true for a stock that’s faced with a bimodal (yes or no) event. In the Altria example, its court case would determine the future of the company. If it resolved in Altria’s favor, the stock price would soar higher. If it resolved against Altria, the price would crater. This is a bimodal event where it’s actually a low likelihood that the future price will stay near the current price. The probability distribution in this case is bimodal and looks more like this:

If an options contract misprices this bimodal outcome by assigning a normal distribution, it’s possible to make a lot of money by betting on a “tail event”. The options contract doesn’t think there’s a high probability that the price will swing wildly, so if it does, there’s large profits to be made.

Jamie Mai deeply understood the power and mispricing effects of these normal-to-bimodal distribution events. It’s a theme you’ll see throughout the next two trades.

Trade #2: Capital One Financial (COF) Calls

In 2002, Capital One (COF) had significant exposure to the subprime market. This was fine at the time because everyone assumed COF was a rock-solid business. But then news broke that regulators forced COF to raise its reserves and institute more stringent lending processes.

This news cast doubt on the company's previously held reputation as a leader in subprime credit risk assessment and resulted in a significant decline in its stock price.

Despite this bearish sentiment, Mai saw an opportunity in COF’s out-of-the-money options market. He believed that the market overreacted to the news and that the calls were significantly underpriced.

Jamie Mai thought COF would have a bimodal outcome. The stock would either skyrocket or crater due to its subprime situation. Here’s how he felt about the trade (emphasis added):

“We thought buying the out-of-the-money calls provided the best way to express the trade because the potential bimodal outcome made a large price move much likelier than usual for the stock. Under these circumstances, the out-of-the-money calls were most mispriced and they had more embedded leverage.”

According to Mai, COF’s DOTMs were mispriced and highly leveraged, meaning that the slightest change in market sentiment or price would generate monster returns for those options.

Specifically, they were interested in buying the January 2005 $40 calls, which were trading near $5 at the time.

Before Mai could buy the DOTMs at $5, more bearish news hit the stock, and COF traded to around $27. This caused the calls to drop from $5 to $3.50, making the potential profits in the trade look even more significant. So he bought it for $3.50.

Mai’s bet proved correct. COF recovered and regained its status as a high-quality subprime lender. The stock also fully recovered. Mai held his options for over a year and made six times his money.

Mai exploited the normal-to-bimodal distribution here. COF’s stock price historically traded along a normal distribution until a single event – the subprime lending scare and reserve requirements – dramatically shifted sentiment towards a binary (yes or no) outcome.

It was either yes, COF is a low-quality bank with abhorrent lending practices and inadequate reserves… or no, COF is a solid bank with enough reserves that happened to have a few too many subprime loans on its books in the short term.

“Heads, I win huge. Tails, I lose a little.”

Let’s dive into the final trade example.

Trade #3: South Korean Stocks

South Korean stocks were dirt cheap in 2003-2004. Even though South Korea had done a better job than many of its Asian neighbors in adopting fiscal and market reforms after the 1997 currency crisis, its stock market continued to languish. It didn’t make sense, so Mai dug deeper.

Jamie Mai personally visited South Korea, connected with local buy/sell-side analysts, and had an interpreter translate Korean financial statements. That’s when Mai discovered just how cheap some of these stocks were. Here’s how he explains it from the book (emphasis added):

“There were companies with market caps of $300 million, no debt, and $550 million cash on the balance sheet, which was expected to increase to $650 million in the following year. In this case, there was tremendous asymmetry simply because these companies had nowhere to go but up.”

In other words, you buy companies for less than the cash value on their balance sheets — true Ben Graham net-net situations. And as long as these companies didn’t go bankrupt, Mai would make a killing. The market would realize that these businesses were worth significantly more than their net cash and their shares would double or even triple.

This isn’t an options trade, but we can still see the bimodal nature of Mai’s bet. A stock that trades below the cash value in its bank account, less any outstanding bets, is the Market’s way of saying, “We don’t think this business will survive six-to-twelve months from now.”

That’s a bimodal yes-or-no bet. The company either goes bust or it survives. Prices were so low that the market already tipped its cap as to which bimodal probability tail it chose, which was bankruptcy. Mai took the other side of the trade because he realized that though these companies traded below cash value, they actually generated positive operating profits.

Mai made a killing when the market realized these companies wouldn’t fail and subsequently revalued them at prices significantly higher than the residual cash in the bank.

To sum it all up, Jamie Mai's approach to investing is focused on three key tenants:

Finding mispriced, battleground situations that don't really make sense

Using long-term options to express a specific view

Buying the cheapest thing you can find, whether it's out-of-the-money options or undervalued stocks in Korea

These strategies helped Mai generate Hall-of-Fame returns and land him an interview in Market Wizards.

If you’re interested in learning more about these strategies and how to implement them, check out our detailed DOTM Guide. It has everything you need to learn how to trade just like Jamie Mai and Cornwall Capital.

By clicking here, check out our free guide covering lessons from the greatest macro traders.