Thoughts On Hedging Uranium Exposure

Hedging uranium was a thought experiment that I've been wrestling with for months. While I'm very bullish the long-term fundamentals, I can't help but see the short-term overbought hysteria that's all over Twitter/X. Uranium guys doing victory laps, people shouting for $200-$300/lb spot prices. Cramer talking about it on CNBC. It got me worried.

So I wrote this piece for our Macro Ops Collective members on January 10, 2024. Consider it my stream-of-consciousness for how I'm thinking about hedging this trade. Please let me know if you have any feedback on how I'm thinking about it. Would love to engage in further discourse.

I hope you enjoy.

We’re up ~8R on our uranium (U.UN) position, with prices up almost 100% from our original entries.

At some point – I can’t tell you when – we will experience a significant drawdown in that position. Here’s why I’m so confident.

We’re seven months into this bull trend without a single bear bar. This is what happens during parabolic price moves.

On the one hand, I shouldn’t worry about the short-term mark-to-market drawdown as the long-term uranium bull thesis remains solid. Supply continues struggling, and utility companies (read: forced buyers) will eventually buck up and pay $100/lb to keep the lights on.

But on the other hand, I am sort of worried about the drawdown because I haven’t found a straightforward way to hedge our long exposure.

Let’s start from first principles. We’re long the physical commodity. How do you hedge long physical exposure?

Usually, in liquid markets like copper or oil, you buy futures puts. So you’re “long” the futures contract but cap your downside by buying long-dated puts on some two-sigma negative event price.

Or you sell calls on your long futures position. This effectively reduces your cost basis while keeping you in the trade (I discussed this strategy with Albert Ayuso on my podcast two weeks ago).

Those are great strategies in liquid markets. But uranium doesn’t have a liquid futures market. I can’t sell calls or buy puts on physical uranium.

There’s not even an options chain for U.UN. So even if we wanted to sell calls or buy puts to hedge, we couldn’t.

Which makes hedging hard (if not impossible) in the traditional sense. I see two unconventional potential hedging strategies.

Hedging Strategy 1: Short Expensive Miners With Deteriorating Technicals

One option would be to find the most expensive uranium producer with the worst chart and short on a technical breakdown.

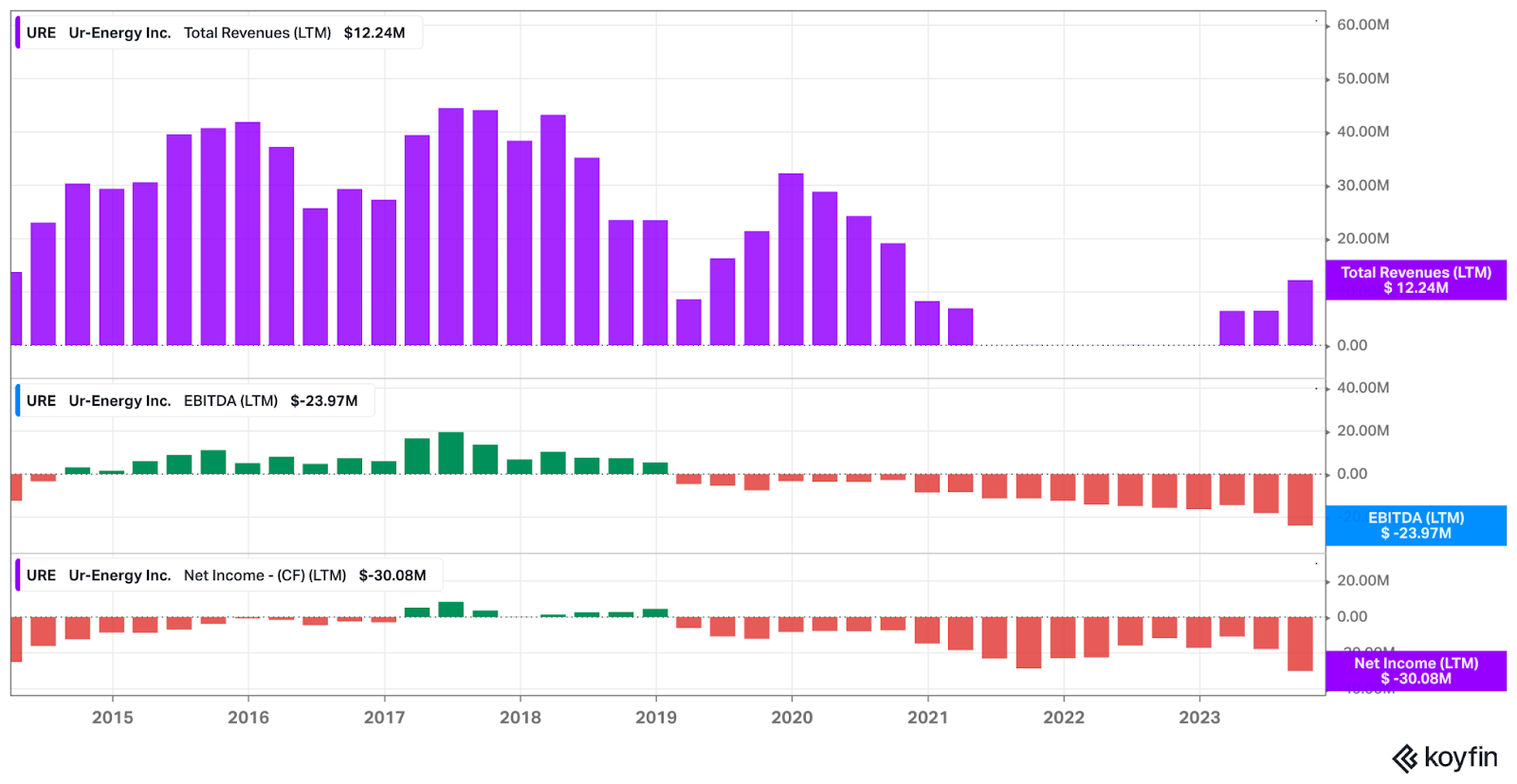

Take Ur-Energy (URE.TSX), for example. URE is a small producer with 12 projects in the US (mainly Colorado).

The company has a CAD 561M market cap and a ~CAD 500M EV. Over the past ten years, URE's highest EBITDA year was ~$20M in June 2017 (LTM).

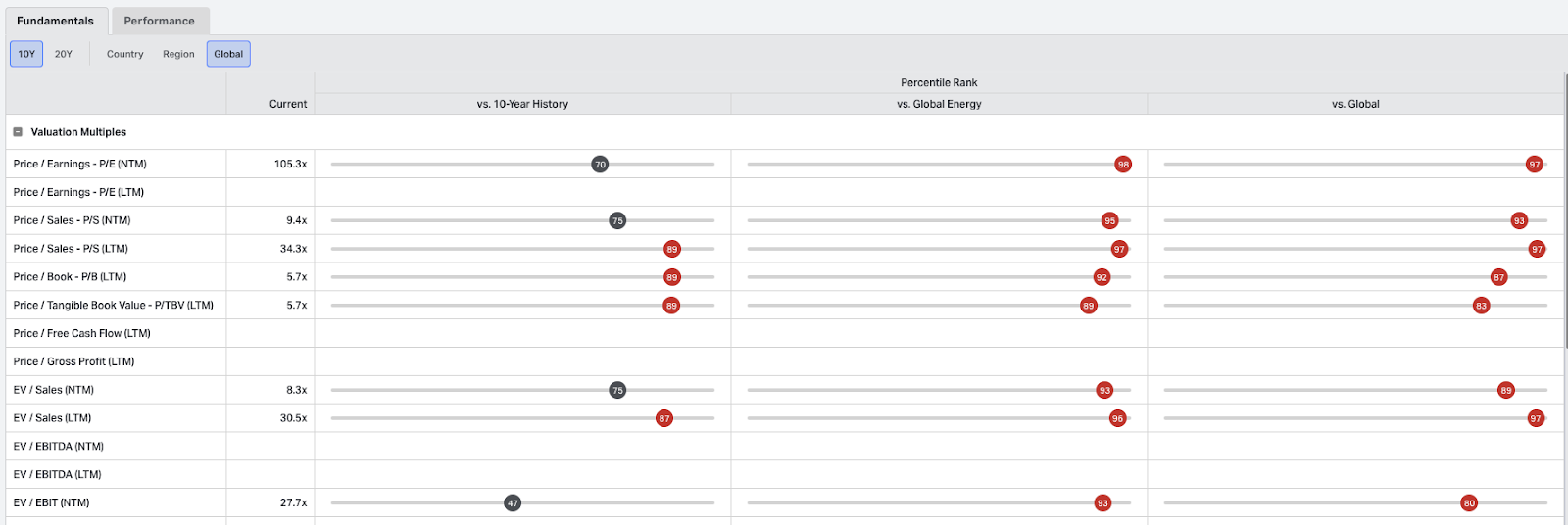

In other words, you’re paying ~25x peak EBITDA for a producer exposed to cost inflation, permitting issues, ESG issues, and serial share dilution. In fact, URE is one of the most expensive stocks by any valuation metric (see below).

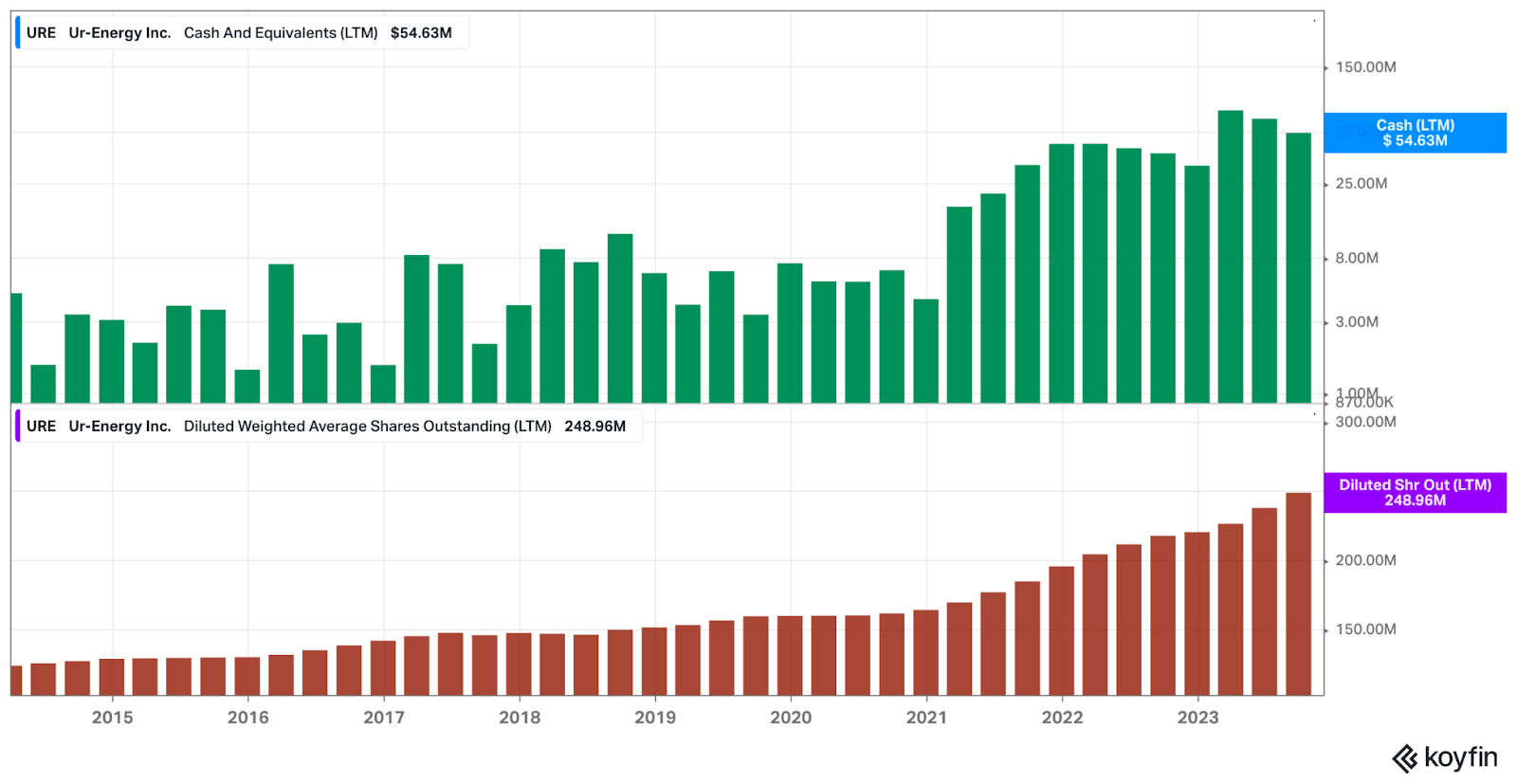

And sure, URE has net cash on the balance sheet, so it's not as bad as it could be. But they’ve generated that cash through share issuance, not business operations (see below).

So you have a company that’s never generated more than $20M in EBITDA, whose only real money-making strategy over the past ten years is issuing shares to suckers willing buyers.

At its current pace, URE will run out of money within the next 18 months. That won’t stop it from trading higher on positive uranium news. But that’s where I think the hedge comes in.

You fade any price spike on non-company-specific news to hedge your physical exposure in U.UN, which should benefit more directly from positive commodity news.

That’s one idea. Another idea in the same “short an expensive producer” theme is a company like Cameco (CCJ).

CCJ is like URE in that it’s one of the most expensive stocks globally.

But it's unlike URE in every other way. CCJ has generated ~$2B in revenue on average over the past decade and even averages an operating profit of $36M.

The company is one of the world’s largest uranium producers in a suitable jurisdiction. Don’t get me wrong, this is an excellent asset to own over the long term. But we’re trying to hedge here, so how can we make this work?

Let’s go back to valuation. CCJ is expensive against its 10-year history, the global energy sector, and the entire universe of stocks.

We also know that most companies revert to their historical averages over time. Even the world’s best mines. Here’s what mean reversion looks like for CCJ.

Historically, CCJ trades at an average EV/Sales of 4.2x, an average EV/EBITDA of 16x, and an average EV/GP of 13x.

As the chart above shows, CCJ currently trades at or two standard deviations above its historical averages.

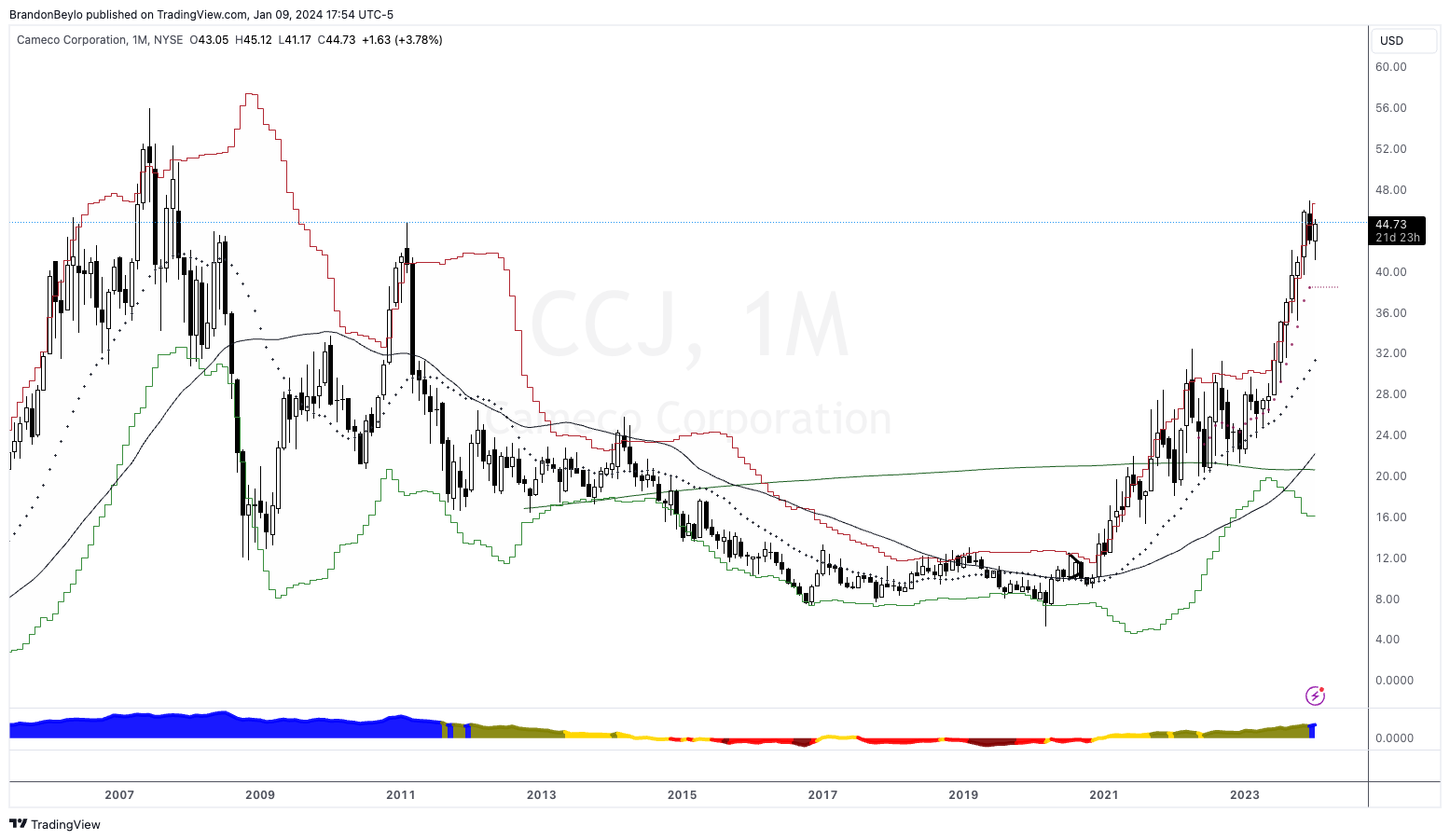

Let’s head to the monthly chart.

This chart is interesting for two reasons. Prices are hitting the prior 2011 high, which now acts as resistance.

And two, the SQN just hit Bull Volatile this month. The last time CCJ hit Bull Volatile was its major top in 2007 / 2011.

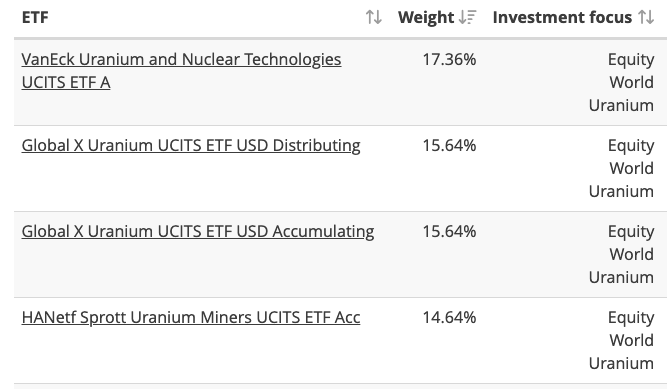

However, there are tons of headwinds to this hedge trade. CCJ is the most liquid way to play the “long uranium producer” thesis (outside Kazatomprom). And it has a ~15% weighting in any liquid uranium ETF (see below).

Net inflows into any of the above ETFs will act as price support. Then there’s the argument that “you pay a premium for a safe asset in a safe jurisdiction.”

Fine. But it’s still mining.

CCJ faces the same cost pressures and regulatory burdens as everyone else. Should it really trade at two standard deviations above the mean into perpetuity?

I’m working with Octavio on finding potential put contracts at varying strikes and duration. If you have any ideas, let us know in the Slack.

That’s Strategy 1. Let’s examine Strategy 2.

Hedging Strategy 2: Taking Partial Profits In U.UN To Recycle Into Yellow Cake (YCA)

On the surface this looks nothing like a hedging strategy. We’re taking profits in something that tracks spot uranium just to buy another thing that follows spot uranium?

Sort of.

Yellow Cake (YCA) is different than U.UN in that it’s not a trust. That means someone, like a large uranium producer, can buy YCA and all the uranium pounds in its piggybank.

FT.com wrote about this distinction in a December article (emphasis added):

“Yellow Cake has a 10-year supply agreement with Kazatomprom, the world’s largest producer of uranium, to buy $100mn of the mineral each year from the Kazakh company, which Yellow Cake then holds in storage facilities in Canada and France. At present, Yellow Cake holds the equivalent to almost 20 per cent of annual global supply.

Reflecting the surge in uranium prices, shares in Yellow Cake have rallied 54 per cent this year, taking its market capitalisation to £1.3bn. Last week the company said its net asset value had jumped from $1bn in March to $1.8bn as of early December.

To cash in, the company would either need to sell its holdings of uranium at higher prices than those at which it bought them or be taken over by a utility in need of supply.”

That last part is essential because that’s our hedge. If we just hold U.UN, we don’t have that upside exposure to a utility going, “Hmm .. We’re out of uranium, the mines can’t produce it fast enough. Why don’t we just buy this company that owns 20% of the annual global supply?”

It’s a right-tail hedge because a buyout would result in higher prices (how much higher would depend on the discount to NAV on trading day). But it caps the left tail since we’d take partial profits in U.UN to fund the YCA purchase.

In a perfect world, you take partial profits in U.UN around some local top. Then you wait for a pullback and redeploy those profits into YCA at a much lower price.

But I don’t have a crystal ball, so timing this “hedge” will be difficult.

Conclusion

I’m still playing with these uranium hedging ideas. Writing this Long Pull Report helped me refine some of these ideas. But I want your feedback.

How would you attack this hedging problem? What instruments did I overlook? How would you construct this trade?

U.UN is an 18% notional position, so the portfolio goes wherever the uranium wind blows. Finding a way to properly hedge our uranium exposure could go a long way in preserving gains and reducing portfolio volatility, at least as best we can, while maximizing our long-term return potential.

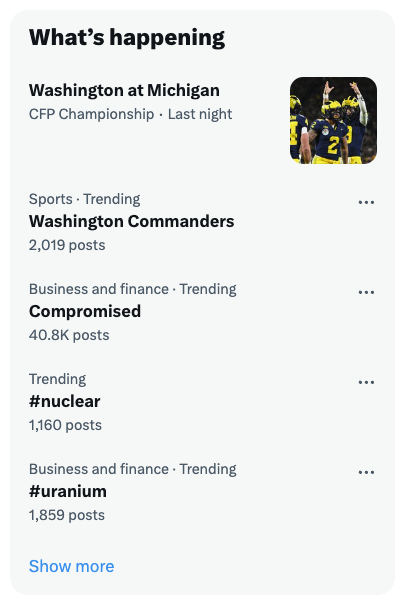

The other reason why I’m thinking about hedging uranium is I’m starting to see more parading from uranium longs. My Twitter/X feed is filled with U308-eyed bulls saying “next stop, $150!”

Uranium was even trending on X last night.

You also have Uranium-specific Twitter accounts highlighting their follower count growth. Again, the long-term picture remains very bullish, supply and demand are still doing their thing.

It’s just you don’t usually see these types of things at market bottoms. That’s why I’m cautious here.

Thanks for reading, and I’ll see y’all next week.